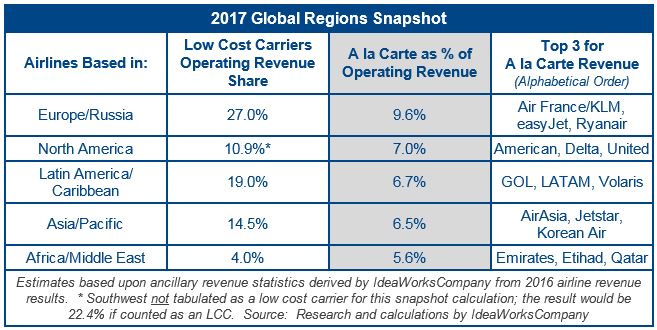

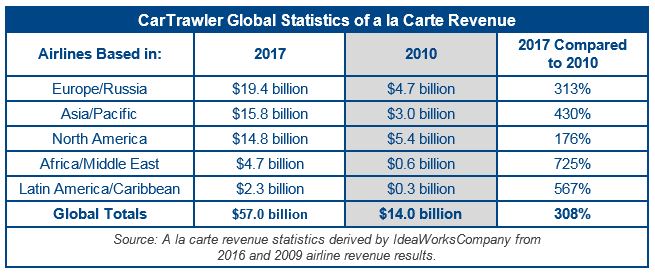

European Airlines Lead 2017 a la Carte Revenue Estimate at $19.4 Billion with Asian Carriers 2nd at $15.8 Billion

Feb 19, 2019

The huge increase of 308% for a la carte revenue since 2010 offers testimony to the growing popularity of the low cost airline model and the a la carte approach to pricing. Be it global network airlines like Emirates in the Middle East, ancillary revenue champions such as AirAsia and Ryanair, and even traditional airlines like TAP Portugal, all are becoming better retailers to encourage consumer spending and to boost returns for investors. Along with this growing retail expertise, car hire and hotel booking capabilities also allow airlines to better serve the entire spectrum of consumer travel needs.

Aileen McCormack, Chief Commercial Officer at CarTrawler